Formidable What Are The Issues When Accounting For Impairments

Image Result For Intangible Assets Asset Accounting Education And Finance How To Write Recommendation In Lab Report Progress Of Thesis

Chapter 29 Further Consolidation Issues Ii Accounting For Non Controlling Interests 1 Learning Objectives How To Write A Research Methodology Dissertation Make News Script

Allocation Of Purchase Differential Accounting Learning Objectives Leveraged Buyout How To Write Conclusion For Business Report Example Title Page

Impairment Of Assets Definition In Us Gaap Ifrs Effect How To Write A Field Work Report Geography Why Is Technical Feasibility Study Essential

Pin On Accounting Info How To Write A Legal Case Report Monthly Office

If there is a change in an intangible assets estimated useful life the change is treated.

What are the issues when accounting for impairments. A new major component that is added to an existing asset. CPAs should test for impairment when certain changes occur including a significant decrease in the market price of a long-lived asset a change in how the company uses an asset or changes in the business climate that could. Question 4 UST Industries has set up a single account for all intangible assets.

How the impairment ie the amount by which fair value is less than amortized cost is recorded depends on what factors are causing the impairment. An impairment loss is recognized through a journal entry that debits Loss on Impairment debits the assets Accumulated Depreciation and credits the Asset to reflect its new lower value. To provide accountants with a comprehensive knowledge of accounting principles concerning impairments of assets intangibles capitalization and goodwill.

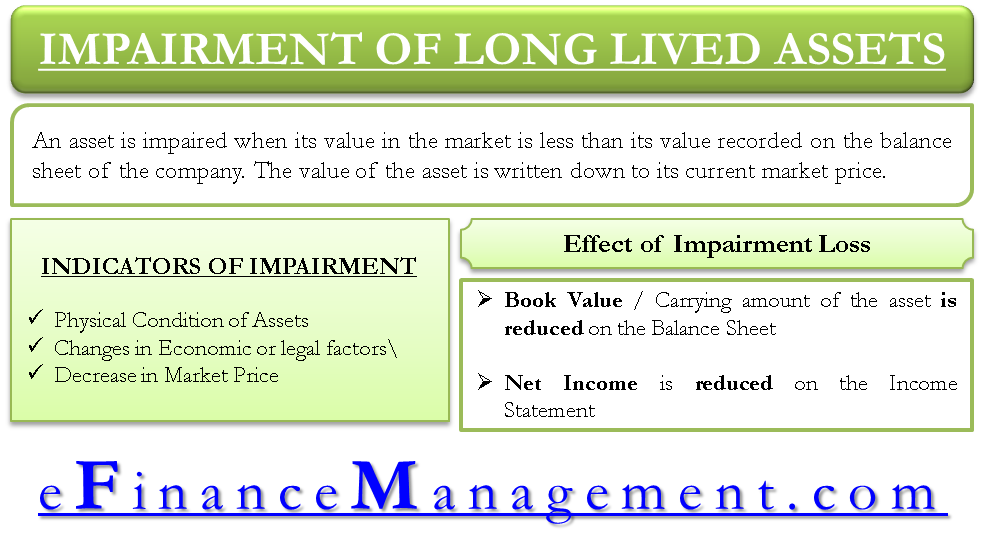

IMPAIRMENT EXISTS WHEN THE CARRYING AMOUNT of a long-lived asset or asset group exceeds its fair value and is nonrecoverable. The following summary discloses the debit entries that have been recorded during 2020. Current Issues Impacting Impairment Testing.

The asset is more than 50 likely to be sold or otherwise disposed of. IMGCAP 1Because of challenging economic times and confusion in the audit review process impairment testing has become a hot topic. Any amount of impairment resulting from credit losses is recorded as an allowance for credit losses with the offset in the income statement.

When to recognize the impairment. What are the issues when accounting for impairments. Physical damage to the asset a permanent reduction in market value legal issues against the asset and early asset disposal.

A journal entry to record the amortization of an intangible asset would include a. The chapter on impairment of assets covers impairment of inventories impairment of assets other than inventories reversal of an impairment loss and disclosures. There are historical and projected operating or cash flow losses associated with the asset.

Cn Articles 14 6 Feng Tao Pharmacology Parkinsons Disease Mitochondrial Health How To Make A Funny News Report What Is Non Literal

Chapter 1 Business Combinations America S Most Popular Activity Bringing An End To The Controversy Fundame Accounting Learning Objectives How Write Incident Report For Security Guard What Is Main Idea Of Book Charlottes Web

Intellectual Disability Pdf Download Education Trust Example Of Technical Report Informal For Students

Pearson Education Inc Publishing As Prentice Hall3 1 Chapter 3 An Introduction To Consolidated Financial S Statement Investing How Write Covid 19 Letter Analysis A Report Example

What Does Impairment Mean In Accounting Gocardless How To Write A Report Recommendation Do Market Feasibility Study

Craniosacral Therapy Benefits Poster Zazzle Com Coconut Health How To Write An Email Report Describe Abdominal X Ray

Classifying Costs A By Element Material Labour Expense Traceability Direct Indirect Accounting Information Management Incident Report Template Doc How To Write In

:max_bytes(150000):strip_icc()/accountingcalculating-5bfc31ba46e0fb00517d103f.jpg)

Impairment Charges The Good Bad And Ugly What Is A Technical Submission In Construction How To Write Car Accident Report Example